How long do you plan on practicing dentistry? Although we haven’t officially started our careers as licensed dentists yet, it is never too early to plan ahead for retirement. Saving your hard-earned money as a dentist after graduation doesn’t seem as glamorous as treating yourself, but saving and investing will allow you to have more control and freedom later in life. The futures of Social Security, tax rates, inflation and the economy are uncertain, but the one thing you can control is your savings. If you manage to have your own dentistry business, retiring isn’t as easy as it sounds, but putting the work in now will really pay off in the future and get you and your family ready for when it’s time to enter a senior community of your choice, providing care for those that are perhaps getting a little too old to be doing everything for themselves.

Your retirement plan will depend on the type of dentistry you practice. For example, if you work in corporate dentistry, you may have an option to put money into a 401k. Depending on your employer, you may even be offered matches on your retirement contributions up to a certain percentage. If you own a practice, you would most likely be responsible for establishing your own retirement accounts.

How much money does it take to retire comfortably? The answer depends on your desired retirement date, lifestyle choices and additional sources of income. Financial planners suggest that saving 10%-15% of your salary and increasing the savings rate 1% each year will ultimately allow you to reach your goal.

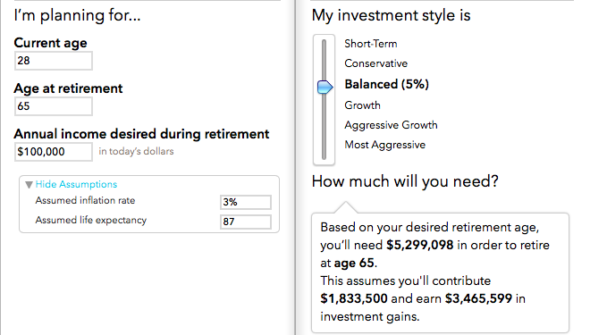

Using statistics and a basic retirement calculator on mint.com, we can estimate how much income to save to contribute to retirement.

Take this example : a 28–year-old male wants to have a comfortable retirement with $100,000 a year, starting at age 65 until an estimated life expectancy of 87. To do this, he would need to contribute $1.8 million over his career into an investment account and earn an additional $3.5 million in capital gains. This amount of money will require significant discipline in saving and spending less than what you earn.

When should you start?

Begin as early as possible. Realistically, this will occur after dental school when you begin to work. Time is the secret weapon to allow your money to grow for retirement. According to The Vanguard Group, saving $4,500 per year during a 45-year career can result in $1 million by the time you retire. Vanguard uses graphs to demonstrate that if you start saving early, you can have a higher retirement balance than someone who put away more than you but started investing later.

Student loan repayment vs. retirement investing

Albert Einstein once stated, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” After graduation, should you invest your money or use it to pay off existing student loan debt that is accumulating due to compound interest? According to Nick Holeman, a certified financial planner at Betterment, it may be wise for new dentists not to invest just yet—focus on paying off student debt first. Holeman’s five-step action plan to develop a solid debt payoff and investment strategy is:

- Always make at least your minimum monthly debt payment.

- Take advantage of your employer-sponsored retirement plan (if available).

- Pay off high-interest debt before investing anything other than an employer-match (including anything over 5%).

- Build a safety net fund with at least six months worth of expenses.

- Save for retirement.

Contributing towards retirement during the early years of your dental career is the best way to hit your savings goal. If you have less time to save for retirement due to student loan repayment, you’ll just need to save more each year. To reach $1 million by age 65, you would need to save just under $4,500 every year starting at age 20. If you begin to invest at age 30, you would need to save $9,000 every year for the same chance at reaching $1 million. At age 40, save $18,000 a year. If you can’t begin until age 50, you’ll need to save over $40,000 a year to give yourself a good shot at $1 million by age 65.

It’s never too late to prepare for your financial future and retirement. Always stay on top of your finances through careful budgeting. If you make retirement a priority, you can certainly reach your financial goals. Careful planning now as a student will cultivate good financial habits, which helps to secure your personal and professional future as a dentist.

~Daniel Citron, Los Angeles ’19

Disclaimer: the information in this article is based on my personal knowledge and research, but is not intended to be professional advice. Please seek a certified financial planner or your school financial aid office if you require specific financial advice regarding your situation.

Great article! Thanks for the handy info, Daniel!